Interest rate risk management

Interest rate risk arises when changes in market interest rates and interest margins influence finance costs, returns on financial investments and valuation of interest-bearing items. The interest rate risk is managed and controlled by Treasury. The interest rate risks are managed through balancing the ratio between fixed and floating interest rates and duration of interest-bearing debt and interest-bearing financial assets. Additionally, Valmet may use derivative instruments such as forward rate agreements, swaps, options and futures contracts to mitigate the risks arising from interest-bearing assets and liabilities. The ratio of fixed rate debt of the total debt portfolio is required to stay within the 10–60 percent range including the interest rate derivatives. The duration of the non-current interest-bearing debt, including the current portion, and the interest rate derivatives is allowed to deviate between 6–42 months.

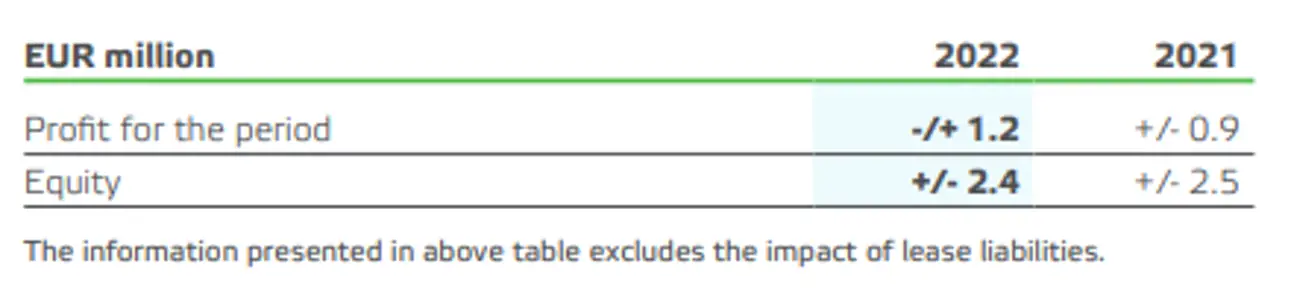

The fixed rate interest portion was 30 percent (44%), the duration was 1.2 years (3.5 years) and the EUR denominated debt was 100 percent (100%) of the total debt portfolio at the end of 2022. The basis for the interest rate risk sensitivity analysis is an aggregate Group level interest rate exposure, composed of interest-bearing financial assets, interest-bearing liabilities (excl. leases) and interest rate swaps, which are used to hedge the underlying exposures. The sensitivity analysis does not include interest component of foreign exchange derivatives since the impact of a one percentage point change in interest rates is not significant, assuming similar change in all currency pairs at the same time. For all interest-bearing debt, assets and interest rate derivatives to be fixed during the next 12 months a change of one percentage point upwards or downwards in interest rates with all other variables held constant would have following effect, net of taxes:

Valmet has used interest rate derivatives to hedge the interest rate risk of its debt portfolio. All interest rate swaps have been designated to cash flow hedge accounting relationships. The nominal and fair values of the outstanding interest rate derivative contracts are presented in Note 9 to Financial Statements 2022.